🚨 RVLV Alert: Undervalued Fashion Play Ready to Revolve Your Portfolio? Inside Scoop on Earnings & Trends!

Welcome to this week's deep dive in our Financial Insights newsletter! Today, we're zeroing in on Revolve Group, Inc. (Ticker: RVLV), the millennial-favorite online fashion retailer that's navigating a tricky consumer landscape. With Q2 earnings just out (as of August 5, 2025), is RVLV a bargain buy or a wardrobe malfunction waiting to happen? We've crunched the numbers, scanned social buzz, and eyed sector shifts to bring you a no-fluff analysis.

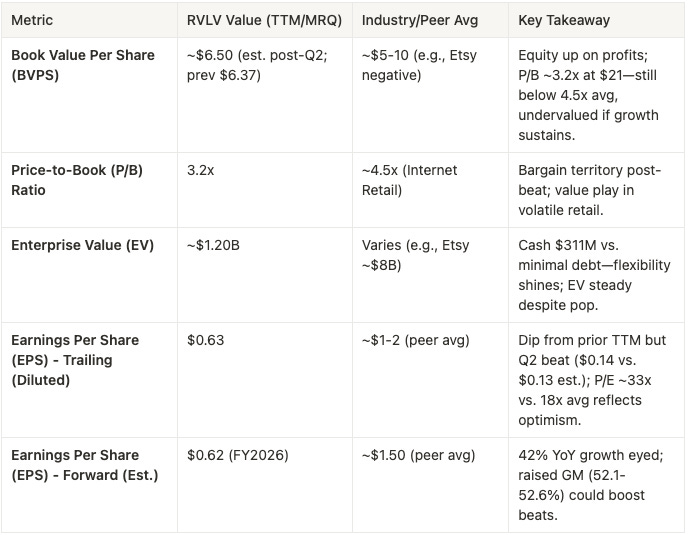

1. Financial Metrics Snapshot

RVLV's Q2 shines in the Internet Retail arena (Consumer Discretionary sector), with sales growth accelerating from Q1's flatline.

Updated TTM figures incorporate Q2: Net sales hit $309M (+9% YoY), gross margin 52.1% (+4 bps), op income $18.8M (+10%).

Cash climbed to $310.7M (debt-free). Peers like Etsy and Stitch Fix lag on growth; RVLV's efficiency edges them out.

Stock at ~$21 post-earnings (market cap ~$1.5B, EV ~$1.2B low due to cash hoard).

New TTM EPS: $0.63 (down from $0.70 pre-Q2, as Q2 '25 $0.14 replaces Q2 '24 $0.21, but beat signals momentum).

Forward EPS est. $0.62 unchanged, but raised GM could lift it.

Float: 40.11M

Short Float: 18.84%

Insider Own: 43.73%

Institutional Own: 66.01% (up 5.4% over last 3 months)

Rel Volume: 2.9x avg

52High: $39.58

52Low: $16.80

Bottom Line: Q2 beat (sales +9%, active customers 2.74M +6%) bolsters resilience, with July sales +7% signaling H2 strength. Undervalued on P/B, premium P/E bets on recovery—watch inventory drop (-6% YoY to $210M) for efficiency gains.

2. Dilution Check: Clean Slate

No changes—zero major dilution events August 2024–2025 per SEC filings. Shares stable at ~71M total (Class A/B). Q2 repurchases: $1.7M (92k shares at $18.78 avg), $55.9M left in $100M program. EPS integrity intact.

3. X Sentiment: Bullish Post-Beat Buzz

X chatter (August 5–6, 2025) flips bullish post-earnings: Mentions highlight "modest beat," "9% revenue growth," and "raised gross margin outlook" (e.g., "$RVLV coming back strong! Nice beat"). Low volume but positive tone—traders note Lazarus-like rebound, with AH +2%. Neutral pre-earnings; now optimistic, though treat as sentiment only (e.g., "EPS $0.14 beats, rev $309M crushes est.").

4. Catalysts on the Horizon

Earnings delivered: Q2 beat (EPS $0.14 > $0.13, rev $309M > $297M), raised FY25 GM to 52.1-52.6% (from 50-52%), Q3 GM 51.2-51.7%. Positive impact—shares up AH; volatility ahead as market digests.

Near-Term: July sales +7%; Q3 earnings ~November—positive if trends hold.

Medium-Term (H2 2025): International +17% YoY in Q2; resale/tech pushes could drive margins higher—positive tailwind.

Wild Cards: Tariffs/inflation noted in guidance; uncertain but mitigated.

Catalysts lean positive, per company release.

5. Sector Vibes: Fashion's Tough Runway

Consumer Discretionary/Internet Retail faces spending cuts (20% expect 2025 improvement, per McKinsey), but resale boom (10% market share, +12% YoY, Fidelity) favors RVLV's DTC model.

Q2 int'l growth +17% outpaces domestic +7%; macro easing (rates/GDP) could lift, but tariffs loom. RVLV's Owned Brands mix boosted margins—opportunities in value trends for upside.

Final Verdict: Closet Upgrade Time?

RVLV's Q2 beat, cash surge, and guidance hike signal turnaround potential in choppy retail. Bullish X shift, undervalued metrics, and growth catalysts make it a solid mid-cap pick (15-25% upside if margins expand). Sector drags persist, but for growth investors, it's a buy-the-dip play—monitor Q3 for confirmation.

Bull Case for RVLV

The bullish outlook centers on RVLV's resilient Q2 2025 performance amid a challenging retail environment, with net sales up 9% YoY to $309M (beating estimates by 4.36%), active customers growing 6% to 2.74M, and international sales surging 17%.

Analysts highlight efficiency gains—gross margin expanded 4 bps to 52.1%, driven by higher Owned Brand mix—and raised FY2025 guidance (GM now 52.1-52.6%), signaling potential for sustained growth. Strong cash flow ($52.4M free cash YTD, +424% YoY) supports buybacks ($55.9M remaining) and a debt-free balance sheet, positioning RVLV for expansion in resale and tech personalization. If consumer sentiment improves with easing rates, bulls see 15-25% upside.

Bullish Price Targets: High-end targets reach $30-36 (e.g., Roth MKM at $36 from Feb 2025, implying ~70% upside from ~$21 post-earnings), with consensus average ~$23 (up ~10%). Morgan Stanley recently raised to $22 (from $19), citing beat momentum.

Romstocks Price Target is $26-30.

Bear Case for RVLV

Bears point to persistent headwinds in discretionary spending, with inflation and tariffs pressuring margins (noted in guidance as susceptible to variability). Despite the Q2 beat, net income fell to $10M from $15.4M YoY due to $8.9M in forex losses and a higher 28% tax rate, while diluted EPS dropped to $0.14 from $0.21. Average order value slipped to $300 (-2% YoY), and domestic sales growth lagged at 7%. If economic uncertainty deepens, bears warn of slowed recovery, with high P/E (~33x TTM) leaving room for downside if Q3 misses.

Bearish Price Targets: Low-end targets at $17-19 (e.g., some holds/sells implying ~20% downside), with average consensus ~$22-23 balancing risks. No immediate downgrades post-earnings, but prior cautions (e.g., BofA at $20 Sell pre-Q2) reflect valuation concerns.

What’s your post-earnings take? Hit reply or comments below.

Subscribe for real-time updates!

Best,

Rom

Romstocks Research

Disclaimer: This is not investment advice and we do own RVLV stock.